Hi, thank you for joining us and welcome to this installment of David W Crossing's clarifying tax situations. What are the common issues that you're going to have to deal with if you're facing IRS collection action? First of all, taxpayers that have unpaid taxes with the IRS or Franchise Tax Board will eventually face collection action by both organizations. Real quickly, both organizations have a way of identifying you if you're a non-filer, that can put you in collection actions. I've got a whole series on non-filers, I won't get into that here, or you can find yourself in a deep hole after facing an IRS audit or some sort of adjustment to your tax returns, either through the office audit, a field audit, or a correspondence audit. But no matter how you face tax debt, it could just be that you haven't been paying enough taxes on an annual basis and a liability has been building up over time. The bottom line in this area is that tax obligations either must be paid or forgiven in some manner. Otherwise, you're gonna face the following: liens, levies, garnishments, penalties, and interest – a vicious cycle surrounding penalties and their trust damaged your credit rating. Perhaps the most important concept, if you get anything out of this video, you're going to eventually get something from the federal government called the final intent to levy notice. At that point, a 30-day clock starts ticking. If you don't file some sort of collection appeal within that time period, you will lose significant rights and be at the mercy of the revenue officer or automated collection services agents. Better after you, you can lose rights to appeal both the underlying tax liability – if you don't agree with the assessments that are sitting there...

Award-winning PDF software

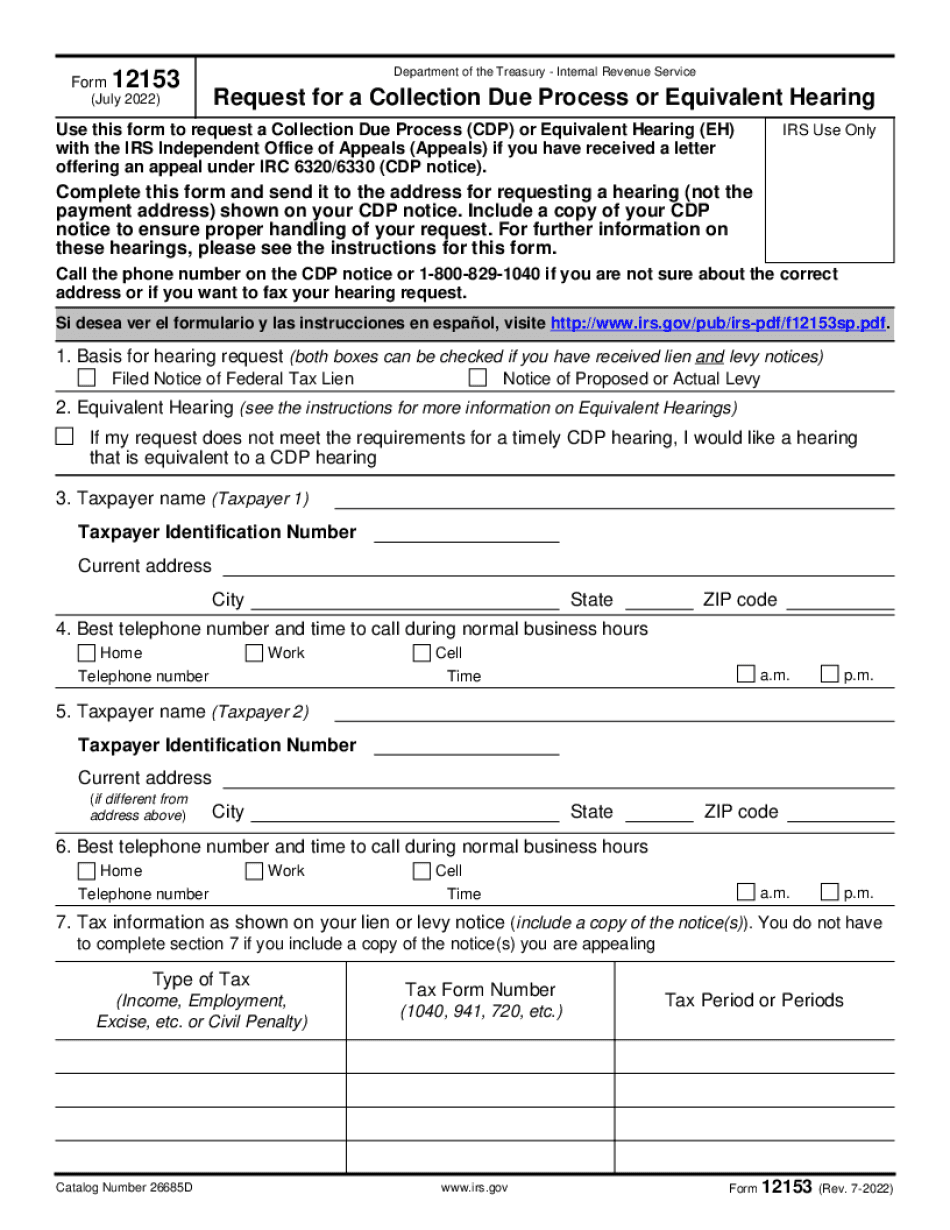

When to file 12153 Form: What You Should Know

Include all the following parts, either in one form or in separate letter: a. The nature of the alleged IRS deficiency; Note : Include proof of the existence of the tax deficiency in Section A on the form if it is required. b. The amount or nature of the deficiency; Note : Include proof of the existence of the deficiency in Section B on the form if it is required. c. The basis for the alleged IRS deficiency; Note : Include proof of the existence of the deficiency in Section C on the form if it is required. d. A statement of your intention to request a Hearing in writing by the posted postmark date. e. A photocopy or print-out of the Notice of Intention to Levy or Lien or Demand for Payment. Include a completed copy of the Notice to the Claimant that was mailed to the last known address. f. Provide supporting evidence of your claim to a deficiency by attaching to the request for a hearing a current copy of the Notice of Intent to Levy or Lien or Demand for Payment that is showing the amount of overpayment. If you did not receive notice of this amount, and that you are able to support your claim, attach a current copy of the Notice to the amount you have claimed and provide your address where you expect to receive notice. g. All information about the person/organization to whom the lien or levy was sent. h. One or two copies of the Notice of Intention to Levy or the Notice of Intention to Lien or Demand for Payment to be provided to the person or organization to whom the lien or levy was sent. i. If you are collecting a debt or claim related to the Lien or Levy and you are not responding to a notice of levy, you must not take any action in connection therewith. (Section D of the lien, levies, or summons) If your liability under the tax is not being disputed, do not take any action in connection with the lien and levy. Section A — D and Section E — H of the notice of levy or summons must also be followed. Section E — H of the notice of levy or summons must be followed. If you are collecting a debt or claim related to the Lien or Levy and you are responding to a notice or summons, you may take any action you deem appropriate in connection therewith.

Online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 12153, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 12153 online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 12153 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 12153 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing When to file Form 12153